Should You Take Out a Personal Loan for Family or Loved Ones?

You might find yourself in a situation when a family member, friend, or loved one asks you for financial help. In many cases, you might be more than willing to offer them a loan or a gift to get them out of a bind.

If you don’t have the money, you might be tempted, or they might ask you to take out a personal loan on their behalf because they cannot get approved for a loan themselves. This is a bad idea and you should avoid taking out a loan for someone else’s benefit.

This article will discuss why you should avoid taking out a loan for someone who cannot qualify for one. It will also offer alternatives that will let you help your loved one.

Why It’s Not a Good Idea

There are a number of reasons why you should avoid applying for a loan for someone who cannot qualify for one on their own.

There’s a reason they can’t qualify

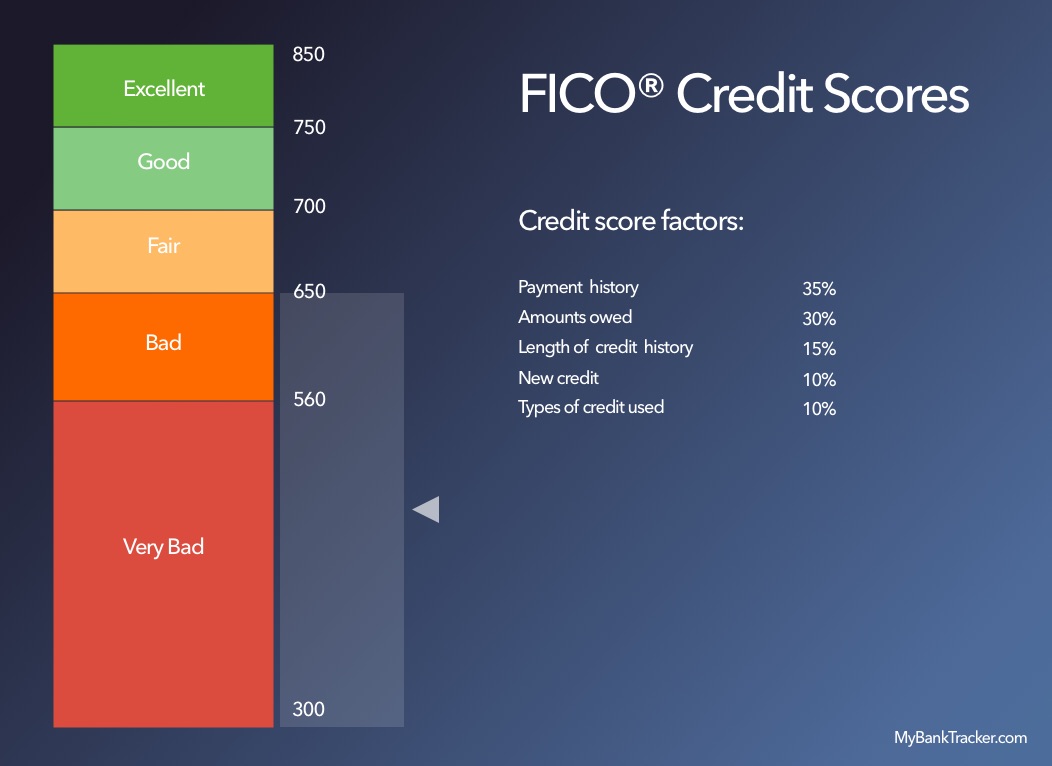

The most basic reason to avoid applying for a loan for someone else is that there’s a reason they can’t qualify for a loan. Even if you know someone very well, you might not know how well they handle money. If they cannot qualify for a loan on their own, that implies that they have a low credit score, and most likely are already in debt.

By applying for a loan for them, you’re just endangering your own financial situation. If they don’t make payments on the loan, you’ll be on the hook for the full amount of the loan that you applied for.

It may jeopardize the relationship

You might have a great relationship with your loved one, but matters of money can get ugly very quick. You don’t want to wind up in the position of bill collector, asking your loved one for payments every time you see them. That can easily lead to resentment as they try to avoid seeing you and paying you back what they borrowed.

Similarly, if you are lenient and wait for the person to pay you back of their own volition, you might become angry when they are slow to pay you back. Especially if you see them spending money in a way that you consider frivolous, without making regular payments to you. It’s not hard to resent someone who owes you a lot of money who doesn’t seem to care to pay it back.

Even if you’re just trying to help someone, it’s very easy for a loan to cause anger and resentment on both sides of a relationship.

Estimated Interest Personal Loan Calculator

Endangering your own finances

When you apply for a loan, you promise to pay back the full amount of the loan over time. If you don’t, the lender will send bill collectors after you and your credit score will decrease.

It doesn’t matter who actually gets the money. Because you signed your name on the loan documents, you’re the one who will be on the hook. If the person you borrowed money for stops paying you, you’ll have to make the loan payments out of pocket. If you don’t, your credit will take a hit and the account will be sent to collections.

Having a low credit score makes it hard to qualify for loans. It also increases the interest rate on loans you do qualify for.

You don’t want to find yourself in a situation where you have to pay someone else’s loan out of your own pocket or face a hit to your credit. In either case, you’ll take a financial hit.

Avoid Cosigning as Well

All of the above dangers apply to co-signing on a loan as well as applying for a loan for someone. When you cosign on a loan, you become equally responsible for that loan.

Having a cosigner can help someone with poor or no credit qualify for a loan, but it is dangerous for the cosigner because they’ll have to make payments if the borrower doesn’t. That’s why most people only cosign on loans, like student loans, for their children or spouses who don’t have a credit score yet.

Alternatives

Even if you don’t apply for a loan on your loved one’s behalf, there are still things you can do to help them.

Suggest a secured personal loan

Many personal lenders offer secured personal loans. Unlike normal personal loans, secured personal loans require that you offer some form of collateral to qualify. If you fail to make payments, the bank will repossess the collateral to make up for its loss.

The collateral provided can be anything of sufficient value. Many banks require a CD or savings account holding a certain amount, title to your car, or something similarly valuable as collateral. The fact that the bank can repossess the collateral means the bank takes on much less risk. This makes secured loans far easier to qualify for. Even someone with poor or no credit can get a secured personal loan if they can offer collateral.

If you’re generous, you can offer to provide some or all of the collateral as a gift. This lets the person get the loan in their own name, and saves you the hassle and resentment of chasing them down for payments.

Pro vs. Cons of Secured Personal Loans

| Pros | Cons |

|---|---|

|

|

Offer to pay them for work

If you’re in a situation where you have some jobs that need doing and don’t mind paying someone, ask your loved one to help out. You can offer to pay them to help you move, do yard work, or something else. You get value out of their help and they get some of the money they need to meet their financial need. This avoids all of the pitfalls of taking out a loan for them without flat out giving them the money.

Personal Loans for Those Without Good Credit

Even if someone has bad credit, that doesn’t mean there’s no way for them to qualify for a personal loan. Secured personal loans are a great way for people with bad credit to borrow money when they need it. Some lenders specialize in offering secured loans, but there are also lenders who are more likely to offer unsecured loans to people with bad or fair credit.

Three of the best lenders for people with bad credit are Upstart, Avant, and OneMain Financial.

Upstart

Upstart is an only personal lender who looks at more than your credit score when making a lending decision.

When you apply for a loan with Upstart, you have to provide the usual information: income, proof of employment, and the like. What Upstart also asks for is information about your education and employment history. If you have a history of steady employment and studied an in-demand field, Upstart will take that into account when you apply for a loan. You might qualify for a loan at Upstart when other lenders won’t give you a chance.

Upstart offers loans of $1,000 to $50,000, so your loved one can borrow exactly as much as they need. Three and five-year payment terms are available.

Upstart Personal Loans Pros & Cons

| Pros | Cons |

|---|---|

|

|

Avant

Avant is another online personal lender that offers loans for people with good or bad credit. If your loved one has bad credit, they still may be able to qualify for a loan, they’ll just have to pay a significant amount of interest.

The benefits of Avant are that you can borrow $2,000 to $35,000 for terms of 24 to 60 months. That gives borrowers a lot of flexibility when it comes to paying the loan off. As a bonus, Avant can send the cash to your bank as soon as the next business day, make it a good lender for financial emergencies.

Avant Personal Loans Pros & Cons

| Pros | Cons |

|---|---|

|

|

OneMain Financial

OneMain Financial is one of the oldest personal loan companies in the US and has been providing loans for more than a century. It operates online and in nearly 1,600 physical locations. You can borrow any amount between $1,500 and $25,000 with loan terms of 24, 36, 48, or 60 months.

One of the perks of working with OneMain Financial is that you can get rewards for paying your bill on-time. Every on-time payment earns rewards points. You can use those points towards gift cards and other rewards. You’ll also get access to discount programs through OneMain Financial. You can save on electronics, appliances, travel, and more.

OneMain Financial offers loans with a huge range of interest rates, so it can take the risk by lending with someone with bad credit. Encourage your loved one to choose a loan amount and term that results in a monthly payment they can handle.

OneMain Financial Unsecured Personal Loans Pros & Cons

| Pros | Cons |

|---|---|

|

|

Compare it with other lenders:

Conclusion

It’s not uncommon for a family member or loved one to ask you for help in times of need. Just be careful of taking out a loan to help them. Instead, look for alternatives to help them get the money they need. Applying for a loan on behalf of someone else can be bad for your finances and bad for your relationship.