Which Credit Report Does Citibank Pull?

- Citi most commonly pulls credit reports from Experian, but the bureau used can vary by state, so knowing which one is relevant to you is important.

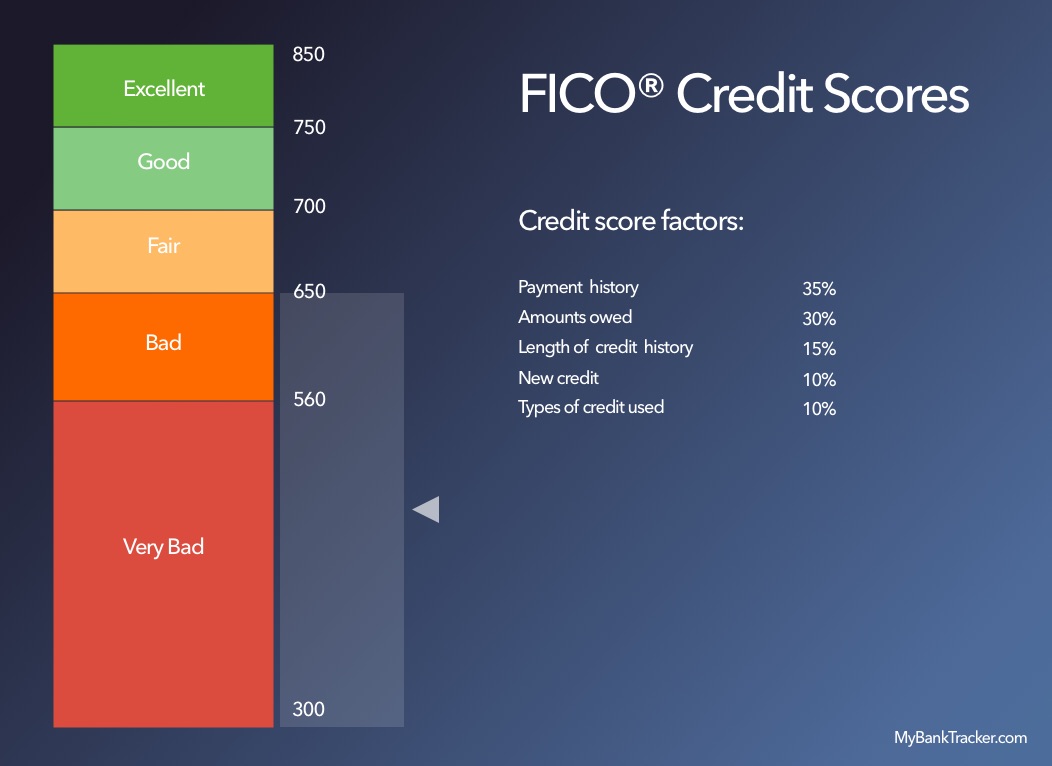

- Improving your credit involves paying down debt, correcting errors on your report, and maintaining a healthy credit utilization ratio (using less than 30% of your available credit).

- Beyond credit score, Citi also considers your income and overall financial health when evaluating loan or credit card applications.

If you’ve ever applied for credit or a loan, it’s a feeling you’ll know well. Submit your application, hold your breath, hope that it goes through as you wait for a response. Yay or nay, accept or reject; it could be either one.

Whatever your outcome, do you ever wonder where a lender, bank or credit card company gets their information to make a credit decision on you? They’ll confer with the three big credit reporting bureaus that record and compile all your credit activity — good and bad.

Citi, for example, uses information from all three agencies but refers most to Experian as the preferred agency for pulling credit checks on prospective customers. We analyzed 211 consumer-reported credit inquiries over the last two years and found that in most cases, Experian is the most commonly used U.S. credit bureau by Citi.

Note: Citibank is a retail banking division of Citi, which is the division that focuses on credit cards and or other non-mortgage consumer loans. It’s a small distinction, but many people tend to interchange the two.

While we strive to identify the credit report most likely to be selected in your case, the fact is that it can vary by state. That’s why we put together a list of the credit reporting data for Citi customers by state. So, you can use it for reference to see which credit report is most relevant to you.

Citi Credit Reports Data

| State | Credit bureaus used |

|---|---|

| Alabama | Experian |

| Arkansas | Experian |

| Arizona | Equifax, Experian*, and TransUnion |

| California | Equifax, Experian*, and TransUnion |

| Colorado | Experian |

| Connecticut | Equifax* and Experian |

| Delaware | Equifax |

| Florida | Equifax and Experian* |

| Georgia | Equifax* and TransUnion |

| Hawaii | Equifax |

| Illinois | Equifax*, Experian, and TransUnion |

| Indiana | Experian |

| Iowa | Experian |

| Kansas | Equifax |

| Kentucky | Equifax* and Experian |

| Maryland | Equifax, Experian*, and TransUnion |

| Michigan | Equifax* and Experian |

| Minnesota | Equifax |

| Nevada | Equifax and Experian* |

| New Hampshire | Equifax and TransUnion |

| New Jersey | Equifax and Experian* |

| New Mexico | Experian |

| New York | Equifax, Experian*, and TransUnion |

| North Carolina | Equifax* and Experian |

| Ohio | Equifax and TransUnion |

| Oklahoma | Experian |

| Oregon | Equifax and Experian |

| Pennsylvania | Equifax, Experian*, and TransUnion |

| South Dakota | TransUnion |

| Tennessee | Equifax* and TransUnion |

| Texas | Experian* and TransUnion |

| Utah | TransUnion |

| Virginia | Equifax and Experian* |

| Washington | Equifax, Experian, and TransUnion |

| West Virginia | Equifax |

| Wisconsin | Experian |

*Denotes the most commonly used credit bureau in the state.

How (and Where) We Found the Data

Banks, lenders and credit card providers are a mysterious bunch. They don’t like to reveal where they pull your credit from. The data we researched from CreditBoards.com was made publicly available by consumers who also applied for credit through Citi, a site where people can submit the results of their credit applications.

The data we found gave some thorough insight into Citi’s preference for using Experian over TransUnion and Equifax over the last two years. (Even though results reach back further.)

Why It Matters

Simple. We want you to confirm which credit reporting agency Citi uses for credit checks, so you can improve your credit standing through that particular bureau — in this case, Experian.

With that knowledge comes power; the power to take control of your credit, and to take the steps to strengthen your credit history and your credit score. Too often, applying for credit means not knowing your score or the contents of your credit report, but submitting an application anyway and hoping it’ll stick. If you guess and assume your credit is strong enough to be approved for a line of credit (even if it is excellent), you’re taking a chance without really knowing where you stand.

By checking your credit, knowing where you actually stand, and knowing which credit agency that banks like Citi check, you can make concerted efforts to raise your credit, and improve the likelihood of credit approval.

Check Your Credit

Checking your credit isn’t some clandestine, covert mission that requires a bunch of secret info, a plethora of PINs and passwords — or worse, money. Checking your own credit is absolutely free and as simple as making one request. You can visit AnnualCreditReport.com for a copy of your current credit report, compiled from Equifax, TransUnion and Experian.

My preferred method is to download a credit-monitoring app, where you have access to your current credit score and report at all times, from multiple credit reporting agencies, updated weekly.

Important note: Checking your credit will not, repeat, will not harm your credit score, so don’t be afraid of pulling your report. When a bank (say Citi) checks your credit, it counts as a “hard” pull that can cause your FICO score to drop a few points. But checking your own credit is a “soft” pull, and won’t affect your score in the slightest.

Pulling your own credit is simple and relatively quick, but remember to stay vigilant and keep an eye out for some details that could complicate the process.

Before hitting ‘submit,’ make sure all of the personal and financial information you enter on your credit report application is correct. A misspelled last name or wrong Social Security number could lead the application software to stop you from proceeding, delaying the process.

Always double check your information.

Beware of trick questions you may be asked, and don’t persuade yourself to pick an answer for the sake of picking; choose “none of the above” if you’re asked if you’ve lived at any of several addresses, but you haven’t. The application verification process often contains trick questions that may not apply.

Always print out your credit report after retrieving it. This can help you compare and contrast it to the next credit report you apply for (you’re entitled to one free report a year), plus, your browser may prevent you from viewing it again if you close out of the page or try to refresh. Having a hard copy on hand helps.

If you don’t feel comfortable accessing your credit report over the web, mail this form to Annual Credit Report Request Service, P.O. Box 105281 Atlanta, GA 30348-5281 for a hard copy, or call 1-877-322-8228.

If you already applied for credit before checking your report, and your application was denied, one start is to ask the bank or lender for a copy of the credit report they conferred in rejecting your request. It’ll list in detail the reasons that contributed to a credit rejection, such as:

- Low credit score

- Not enough credit — both installment and revolving

- Too much active, delinquent or defaulted debt

- Accounts in collections, or recent bankruptcies

Remember that you have a legal right to ask them for your credit report, and they’re legally obligated to provide you with one within 15 days of your request. Then, once you’ve got your report in front of you, in black and white, it’s time to use the info to your benefit and get your credit in the best shape of its life (and yours).

Polishing Your Credit Report

They say you only have one chance to make a good first impression, and nothing could be truer when it comes to your credit. No matter how well-intentioned you are or financially responsible at the core, it’s the immediate appearance of your credit that a bank or creditor will base its decision on. And if yours isn’t the greatest of shape, you could get denied for credit. On top of that, your credit score will take a hit from a hard credit check.

It’s time to give your credit a makeover, especially if your goal is to get approved for credit by Citi, or any other financial providers with high credit standards. Making changes to your credit behavior is a key step since it’ll reflect positively on your credit report. But you’ll also want to remain watchful of your actual credit report because it could contain erroneous or outdated info that can inadvertently hurt your credit against your best wishes.

Here are some steps to take:

Decimate your debt. Paying off as much debt as you can — credit card balances, student loans, car loans or mortgages — shows banks like Citi that you’re responsible; you can borrow money, pay it off in a timely way, and avoid hanging onto too much debt for too long. In short, it supports your creditworthiness.

Look for, and fix, credit report errors. You paid off all that debt from the last bullet point in this list, but it’s still listed as delinquent on your credit report, months and months later. What gives? You did your part, but the credit bureaus haven’t. Or, it could be some other error or mistake, like a defaulted loan in collections that’s not even yours! Your info might be mixed up with someone else’s (like a person who has the same name as you), but now it affects your credit report and score in a very bad way. The moral of the story: Even credit reporting agencies make mistakes, but you also can dispute errors with them. Follow these links to start the dispute process; each credit agency is obligated to follow up with its own investigation:

Strike a balance. To use credit, or not to use credit. That is the question; but what’s the answer? Well, both, actually. Credit is meant to be used but in moderation. Approach your credit limit too close, you risk maxing out that credit card and going into debt — and that leaves a bad impression on creditors who’ll assume you’re too dependent on borrowing money. Use too little credit, and it shows inexperience with borrowing and repayment, not to mention your credit report won’t show any evidence of recent credit activity. Aim to mix it up between revolving credit (day-to-day expenses that vary in cost, like groceries or gas), and installment credit (fixed expenses, like a mortgage loan or car payment).

Increase your credit limit. But don’t spend most of what you’ve added. What’s the point, you might ask? If you have a $5,000 credit limit, and you double it to $10,000, isn’t the money meant to be spent? You could, and if you pay it back in full, on time, no problem. But the way it influences your credit score is more sophisticated than that. By raising your credit limit but spending less, you widen your credit utilization: the amount of credit you use versus the amount available to you. The more credit you have, but the less you spend, paints a picture of someone who isn’t obsessed or reliant on credit to get by. Experts maintain to make use of no more than 30 percent of your available credit; so, if you have a $9,000 limit on your credit card, spend no more than $3,000 a month.

Other Factors to Consider

Credit isn’t the only thing Citi will examine when considering approval. The ratio between your take-home income and your regular expenses count, too — even those you spend through your checking account or debit card. Banks want to see if a. You’re living beyond your means, spending more than you earn (or close to it), and b. That you earn enough money to afford to repay a credit card, a loan, etc. The bank can’t take a gamble without knowing how much cash you have coming in before approving you for credit.

Nobody’s financial situation is perfect, so don’t place too much pressure on yourself to achieve 100 percent credit before applying with Citi. A well-rounded financial situation, a solid credit report, and a credit score in the good-to-very good range (or higher) sets you on the path to showing Citi (and other banks) that you and your credit are a financial force to be reckoned with (and approved for credit, too).