College Grads With Your First Jobs: How to Set Up Your Finances

- Establishing a good credit score early is important for future financial opportunities such as home purchases and car leasing.

- Opening a Roth IRA provides flexibility for retirement by allowing tax-free withdrawals in retirement and permits contributions at any age, which is an advantage over traditional IRAs.

- A 401(k) plan is an additional retirement savings option that may be available from your employer.

Now that you’ve graduated college and landed a job, you can sit back and relax — not so fast!

The real world sneaks up on you all at once, and at times can seem overwhelming.

You’ll be faced with more decisions in the coming months than you’ve most likely made your entire life.

Luckily, there are ways to set yourself up for success, that college professors don’t teach you.

In order to help you take control of your finances, a factor that impacts so many aspects of your life, we’ve done some of the heavy lifting for you.

Here are the first five steps to successful money management. You’ll thank us later.

1. Checking Account

Whether or not you had a checking account in college, you’ll need one now that you’ve landed a job.

Your financial hub

Most employees in the U.S. are paid by direct deposit, so there’s a good chance you will be too.

Direct deposit is a way for an employer to electronically deposit money into your checking or savings account.

You’ll have immediate access to the money once it is deposited to your account each pay period.

In order to set up direct deposit, you’ll need to fill out paperwork provided by your new employer.

This includes bank account information.

So, what if you don’t have a checking account? Now is the perfect time to open one up.

Opening a checking account is the first step to building a strong financial base.

There’s no reason to pay astronomical monthly fees, so it pays to shop around.

If you happen to have a student checking account from college, start by learning about the changes to your account now that you’ve graduated.

Banks are notorious for luring college students in with enticing benefits in order to keep you on as a customer after graduation.

Those exclusive deals and free services most likely ended as soon as you graduated, whether you realize it or not.

What makes a great checking account

At a minimum, you’ll want to know if you’re charged monthly maintenance fees, have minimum balance requirements and if you’ll be charged to use an ATM.

These fees and costs add up, especially since you’re just starting out.

If you’re not happy with the terms of your previous student account or need to open your first checking account, look for a free checking account.

Online checking accounts are worth considering as they usually don’t have monthly fees and come with convenient ATM policies.

Your money is just as safe and secure with any FDIC-insured online bank. The only difference between an online bank (also known as an internet bank) and a traditional bank is that online banks do not have brick-and-mortar branch locations.

Online banks save money by not having bank branches, and this savings is passed on to customers like you.

Some additional benefits of online-only banking can include:

- No monthly fees

- Higher interest rates

- No minimum balance

- ATM fee reimbursements

- Mobile deposits

- Online and mobile banking

- Easy to set up an account online

- Open 24/7

2. Emergency Fund

Everyone should have an emergency fund, even you.

An emergency fund holds money set aside to pay for unforeseen emergency situations.

Having an emergency fund can save you from possible financial ruin.

An emergency fund is only meant to cover a truly unplanned emergency, such as losing your job. Here are some more examples:

- High medical or dental costs not covered by your insurance

- Major car repairs

- Home repairs

- Emergency pet care

- Unexpected travel

Even if you have little to no money to start your emergency fund, it will grow over time.

How much to save

The amount of money you ultimately want to save depends on your monthly expenses.

You’ll want to set a reasonable goal for yourself.

Experts recommend having 3 to 6 of living expenses in an emergency fund.

Ideal Size of an Emergency Fund

| To start… | Ideal goal… | Super safe… |

|---|---|---|

| $1,000 | 3-6 months of essential expenses | 12 months of expenses |

Living expenses include the cost of housing, food, utilities, insurance, transportation, debt and necessary personal expenses.

If saving 3 to 6 months of living expenses is out of your league right now, set a more obtainable goal that you’re comfortable with, such as $1,000.

Having an emergency fund goal doesn’t mean you have to come up with the money overnight. It means that you will work to reach that goal over a period of time.

Maybe it’s a couple of months, maybe it’s a year.

Online savings accounts are ideal

Once you decided on the amount that you’ll aim to save, you’ll need to decide where to save that money.

Open up a savings account for your emergency fund

Out of sight, out of mind.

You’ll want to open up a separate bank account for your emergency fund.

You don’t want to be tempted to use money in your emergency fund for non-emergency events, like a night out on the town.

Similar to opening a checking account, shop around for a savings account that does not have a minimum balance requirement.

Online savings accounts offer higher interest rates with no minimum balance requirements and no monthly maintenance fees.

Find the best rates

Unlock exclusive savings rates and gain access to top-tier banking benefits.

Arrange for direct deposit

You can use direct deposit to help save for your emergency fund.

Often, many employers allow you to divide your direct deposit into multiple bank accounts.

Once you decide how much money to contribute each pay period, talk to your employer to see if this is an option.

Using direct deposit is a great way to automatically deposit money into your emergency fund each time you get paid.

And, you probably won’t even “miss” the money since it will never hit your main checking account.

3. 401(k)

You’re never too young to start saving for retirement.

Even if you’re struggling with student loans or living paycheck to paycheck, investing in your retirement in your 20s is invaluable.

Sign up to participate in your employer’s 401(k) program as soon as you’re eligible.

Typically, you need to be working for several months before you qualify to participate in the program.

You’ll need to fill out paperwork supplied by your company to enroll in the program.

As little as one percent of your money will be automatically deducted from your paycheck and deposited into your 401(k) account.

Get tax benefits

This money is deducted pre-tax. In other words, you won’t pay taxes on the amount of money added to your 401(k) account each year.

You’ll pay taxes on this money once you go to withdrawal it, after retirement.

Check to see if your employer will match your 401(k) contributions.

Essentially, it’s free money that your employer deposits to your 401(k) account each pay period that you participate.

Some employers offer Roth 401(k) plans as well.

The main difference in a traditional 401(k) plan and a Roth 401(k) plan is how the money is taxed. Either now or later.

The money you contribute to a Roth 401(k) plan is taxed now.

You will not have to pay taxes on this type of account when you go to withdrawal from it during retirement.

4. Roth IRA

If your employer does not offer 401(k) benefits, there are other alternatives to saving for your retirement.

A Roth IRA is a retirement account that you open with a bank or financial institution on your own, not through your employer.

You have the freedom to shop around for the best account to meet your retirement goals.

You will have already paid taxes on money earned through your job so money that you contribute to a Roth IRA account is already taxed.

The IRS sets criteria in order for people to qualify to participate. Since you’re under the age of 50, you can contribute up to $6,000 each year to a Roth IRA.

Why a Roth IRA?

A Roth IRA is ideal for savers who expect their income to grow later in life.

With a Roth IRA, you contribute with funds on which you’ve already paid taxes. A traditional IRA allows you to deduct the funds on your tax return.

During retirement, you can withdraw funds from your Roth IRA without paying any taxes on the gains, which saves on taxes if your tax rate is high at the point in time.

With a traditional IRA, you pay taxes on the gains at that point in time.

Traditional IRA Vs. Roth IRA

| Traditional IRA | Roth IRA |

|---|---|

| Contributions may be tax-deductible. | Contributions are not tax-deductible. |

| Pay taxes upon withdrawal. | Earnings can be withdrawn tax-free and without penalties if the funds were in the Roth IRA for 5 years and you’ve reached age 59 1/2. |

| You must be under age 70 1/2 to contribute. | You can contribute at any age. |

| Required minimum distributions (RMDs) are required starting at age 70 1/2. | No RMDs required. |

5. Build Your Credit

With your whole life ahead of you, it’s time to start thinking about establishing credit.

You’ve heard of the term, credit score, but what exactly does that mean?

A credit score is a three-digit number that reflects how likely you are to repay money, known as debt, to lenders, who loan you that money.

Your credit score can affect your life in so many ways, whether you know it or not.

Whether you’re applying for a credit card, buying a home, or leasing a car, lenders check your credit score to determine if you’re eligible to borrow money.

Additionally, your credit score determines the rate at which these lenders loan you money. The lower the credit score, the higher the interest rate.

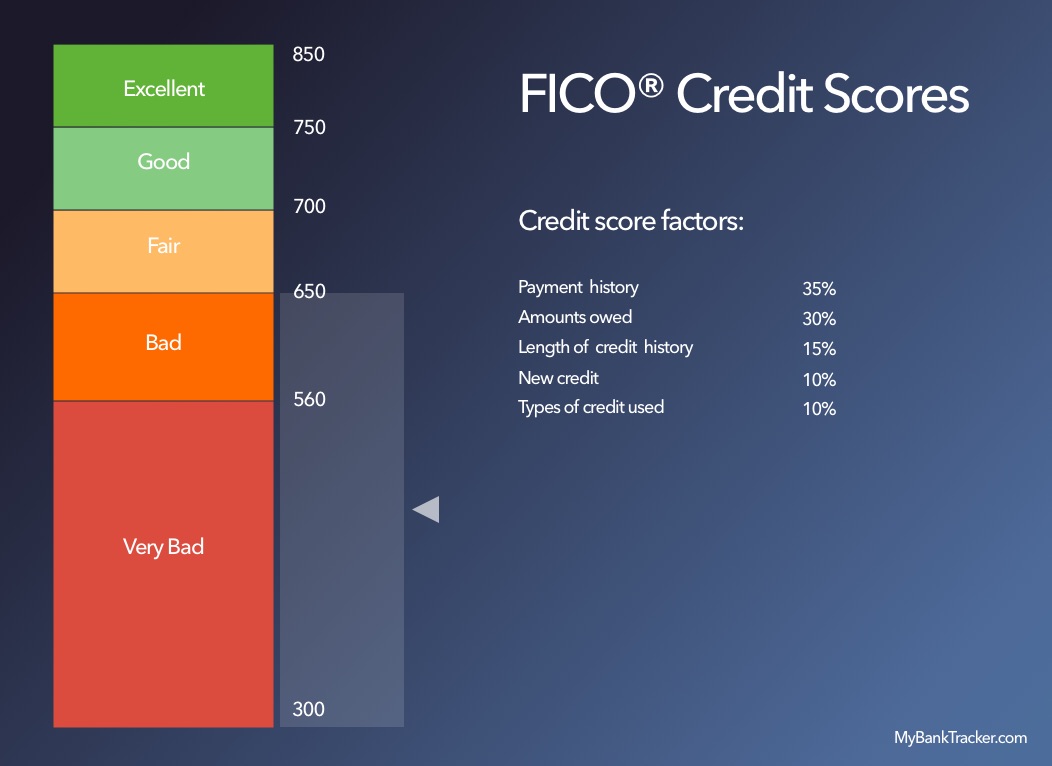

Each person has their own credit score, ranging from 300 to 850.

The most recognized credit score used by most lenders is the FICO credit score. FICO score ranges:

If you’re wondering how your score is calculated, you’re not alone.

Luckily, it’s pretty straightforward.

Since you’re not born with a credit score, and you can’t inherit one, you have to establish one on your own.

One of the best ways (at a young age) to do this is by opening a credit card.

You might be thinking. How can I open a credit card with no credit score?

There’s always a lender out there looking to loan money at an incredibly high interest rate.

Since you most likely don’t have a credit score, your interest rate will be at an all-time high.

Luckily, this only impacts you if you carry a balance month to month.

You can start by applying for a secured credit card.

A secured credit card requires you to put down a deposit in order to qualify for that credit card.

It’s just as easy to establish bad credit as it is to establish good credit.

Never spend more money than you have to pay off the balance and always, always, always, make your payments on time.

Even one late payment can wreak havoc on your credit score.

Conclusion

Now that you’ve set yourself up for success, you’re ready to enjoy this new stage of life.

You don’t want to let irresponsible spending habits take control of your life or be weighed down by debt.

Think of managing your financials as the second most important job.

It takes people years, and some even decades, to fix past financial mistakes.

You don’t have to be one of them.